Definition & Meaning

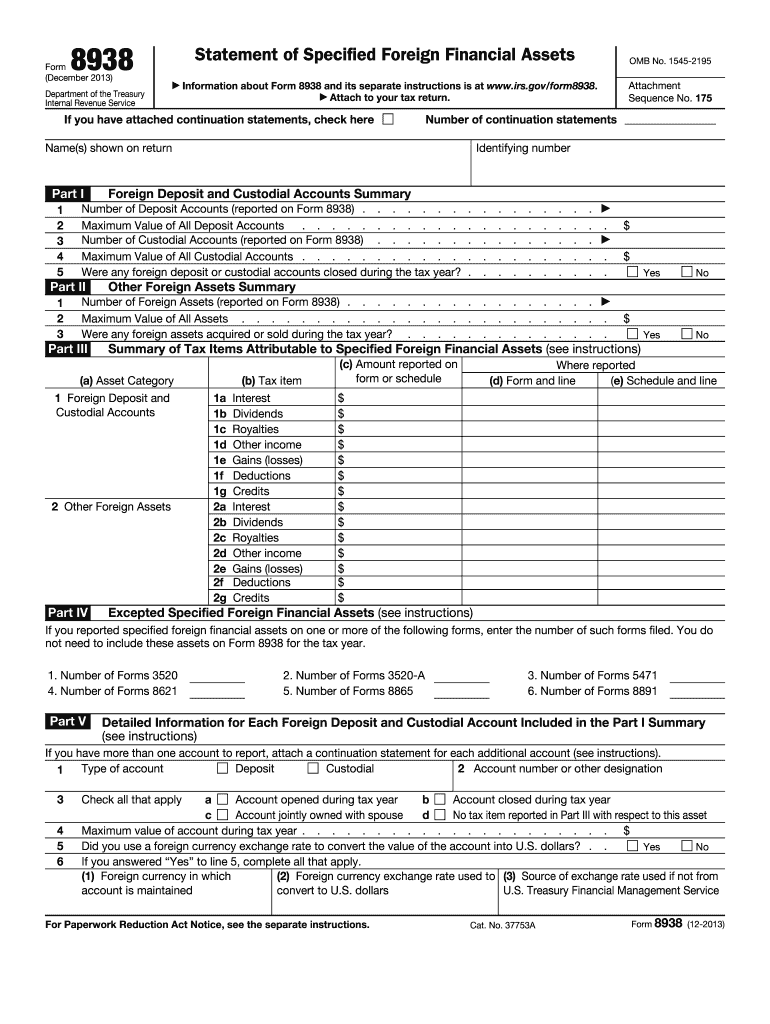

Form 8938, also known as the 2 form, is used by U.S. taxpayers to report specified foreign financial assets to the Internal Revenue Service (IRS). This requirement is part of the IRS's efforts to combat tax evasion through the concealment of foreign assets. Taxpayers must disclose detailed information about such assets, including foreign deposit and custodial accounts, along with other financial assets held overseas.

The form requires taxpayers to report the maximum value of each specified foreign financial asset during the tax year. It also includes sections for reporting any associated transactions throughout the year. Form 8938 is essential for compliance with the Foreign Account Tax Compliance Act (FATCA), which aims to improve transparency and accountability in the reporting of offshore financial activities.

Steps to Complete the 2 Form

-

Gather Required Information: Start by assembling all necessary data regarding your foreign financial assets. This includes account numbers, asset types, and the maximum value held during the tax year.

-

Determine Valuation: Assess the maximum value of each specified foreign financial asset in U.S. dollars. You may need to use the currency conversion rates provided by the IRS for accuracy.

-

Complete Part I: List all foreign deposit and custodial accounts. Include details such as account numbers, financial institution names, and the maximum account value.

-

Complete Part II: Document other foreign financial assets, such as interests in foreign trusts or securities issued by foreign persons.

-

Consider Exceptions: Review Parts III and IV for any applicable exceptions and thresholds that may influence your reporting obligations.

-

Attach to Tax Return: Once completed, attach Form 8938 to your annual tax return (Form 1040) when filing it with the IRS.

Who Typically Uses the 2 Form

Form 8938 is primarily used by specific categories of U.S. taxpayers, including:

-

Individuals: U.S. citizens and resident aliens who have specified foreign financial assets exceeding certain thresholds as of the end of the tax year or at any time during the year are obligated to file.

-

Married Taxpayers: Those filing jointly must consider the combined value of their foreign assets to determine their filing requirements.

-

Business Owners: Sole proprietors, partners, and shareholders of domestic corporations must also account for foreign financial interests when calculating asset values.

Foreign financial asset reporting is not limited to individuals directly holding accounts; controlling interests or signatory authority over foreign assets also necessitate filing Form 8938.

Key Elements of the 2 Form

-

Specified Foreign Financial Assets: Include foreign bank accounts, pension plans, and financial instruments, among others. Definitions and categories are explicitly detailed by the IRS.

-

Asset Valuation: Accurate valuation of assets is critical, requiring taxpayers to convert foreign currency values into U.S. dollars.

-

Reporting Thresholds: Filing requirements vary based on filing status and residency, with distinct thresholds for single, married, and other filer categories.

-

Transactions: Taxpayers must report specific transactions related to their foreign assets, including deposits, withdrawals, and interest or dividend income.

Required Documents

To complete Form 8938, taxpayers should prepare and organize documents such as:

-

Foreign Account Statements: Monthly or annual statements reflecting account balances.

-

Ownership Documents: Records confirming ownership interests in foreign businesses or securities.

-

Appraisals: Valuation documentation for tangible assets held abroad.

These documents facilitate accurate reporting and ensure compliance with IRS requirements.

Penalties for Non-Compliance

Failing to timely file Form 8938 can result in significant penalties. The IRS imposes fines starting at $10,000 for each failure to file, with additional charges accruing if the non-compliance continues after notification by the IRS. Further penalties may be applied if there is a pattern of non-disclosure.

Taxpayers should understand that non-compliance extends beyond financial penalties, affecting future tax return accuracy and potentially leading to criminal penalties if willful non-disclosure is determined.

IRS Guidelines

The IRS provides comprehensive guidance on completing Form 8938. Taxpayers can refer to the instructions attached to the form, which clarify definitions, reporting thresholds, and examples of specified foreign financial assets.

In addition, the IRS frequently updates its guidelines, reflecting changes in reporting requirements and enforcement priorities. Taxpayers are encouraged to consult these resources to ensure full compliance.

Filing Deadlines / Important Dates

Form 8938 must be filed annually, attached to the taxpayer's income tax return. The standard filing deadline aligns with the deadline for Form 1040, typically April 15. Taxpayers can request an extension using Form 4868, allowing additional time until October 15.

It's crucial to note that extensions granted for Form 1040 also apply to Form 8938, but late filing penalties may still accrue if Form 8938 is omitted initially.