Definition & Meaning

The 2012 Form 1065, also known as the U.S. Return of Partnership Income, is a crucial IRS documentation tool used by partnerships to report financial information. Partnerships are unique in that they pass income and associated tax responsibilities to individual partners, rather than the entity itself paying taxes. This form requires detailed disclosure of income, deductions, gains, and losses, which are pivotal for tax compliance and financial transparency in partnerships.

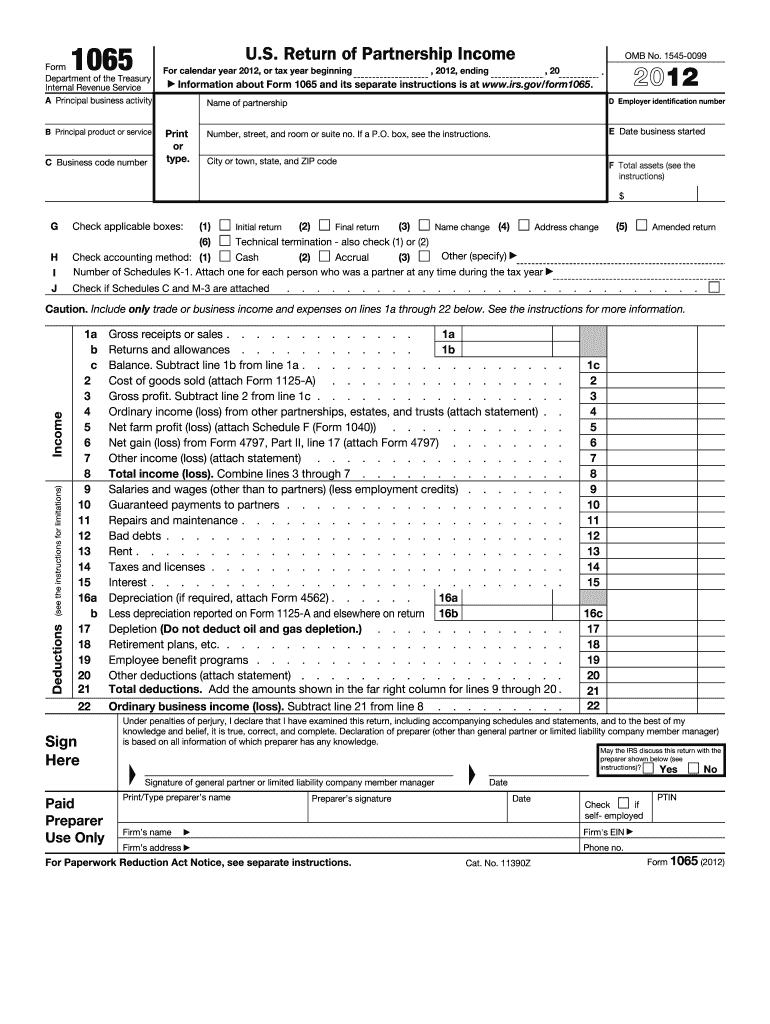

Key Elements of the 2012 Form 1065

Several essential components of the Form 1065 need particular focus:

-

Partnership Identification: Includes details such as the name, address, and employer identification number (EIN) of the partnership, along with the business's principal activity.

-

Income Reporting: Comprised of lines showcasing total income, which includes ordinary business income, interest, and net farm profit.

-

Deductions: Partnerships list deductions here, such as salaries, rents, and depreciation, crucial for minimizing taxable income.

-

Partner Distributions: Information on each partner’s share of the business's profits or losses, requiring meticulous attention for accuracy.

How to Use the 2012 Form 1065

Using Form 1065 effectively involves several steps:

-

Accumulate Financial Records: Gather comprehensive records of all income, expenses, and financial transactions pertinent to the partnership.

-

Understand Sections In-depth: Familiarize yourself with each section, especially items concerning income, deductions, and partner shares.

-

Consult IRS Instructions: The IRS provides instructions specific to Form 1065, ensuring provisions are understood and applied correctly.

Steps to Complete the 2012 Form 1065

-

Complete Basic Information: Input the partnership’s basic identification details on the form.

-

Fill Out Income and Deductions: Enter total revenue in the corresponding sections and itemize all eligible deductions.

-

Report Partner Distributions: Detail each partner’s distributive share of profit or loss accurately on Schedule K-1.

-

Review for Accuracy: Double-check all entries to avoid errors that may lead to penalties.

-

Submit the Form: File the completed Form 1065 using approved methods, ensuring adherence to deadlines.

Filing Deadlines / Important Dates

For partnerships, timeliness in filing Form 1065 is crucial. The standard deadline is the 15th day of the third month after the partnership’s tax year ends. For most partnerships, this date falls on March 15th. Requesting extensions requires Form 7004 and must be submitted before the original deadline.

Required Documents

-

Financial Statements: Including profit and loss statements and balance sheets.

-

Partnership Agreement: To validate terms of partner contributions and profit-sharing.

-

Records of Income and Deductions: Comprehensive lists and proof of all revenues and expenses.

-

Previous Year’s Form 1065: For consistency and accuracy checks.

Important Terms Related to 2012 Form 1065

-

Distributive Share: The portion of income or loss assigned to each partner, reported via Schedule K-1.

-

Schedule K-1: An attachment to Form 1065, critical in portraying each partner’s share of the partnership's income and other pertinent financial details.

-

Ordinary Business Income: Income derived from the partnership’s main trade or business activities.

IRS Guidelines

The IRS issues specific guidelines concerning the proper completion and filing of Form 1065. Compliance with these guidelines ensures the partnership correctly reflects its financial status and fulfills its tax obligations. Critical areas include income attribution, allocation of partner shares, and adherence to reporting standards.

Penalties for Non-Compliance

Failure to submit Form 1065 by the due date results in penalties, typically assessed per month per partner, for each month the form is late. This penalty underscores the importance of timely and accurate filing to avoid unnecessary financial liabilities.

By comprehensively understanding these facets of the 2012 Form 1065, partnerships can ensure compliance, accuracy, and efficiency in their financial administration and reporting processes.