Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send it via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out Promissory Note in Connection with Sale of Vehicle or Automobile - Iowa

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open it in the editor.

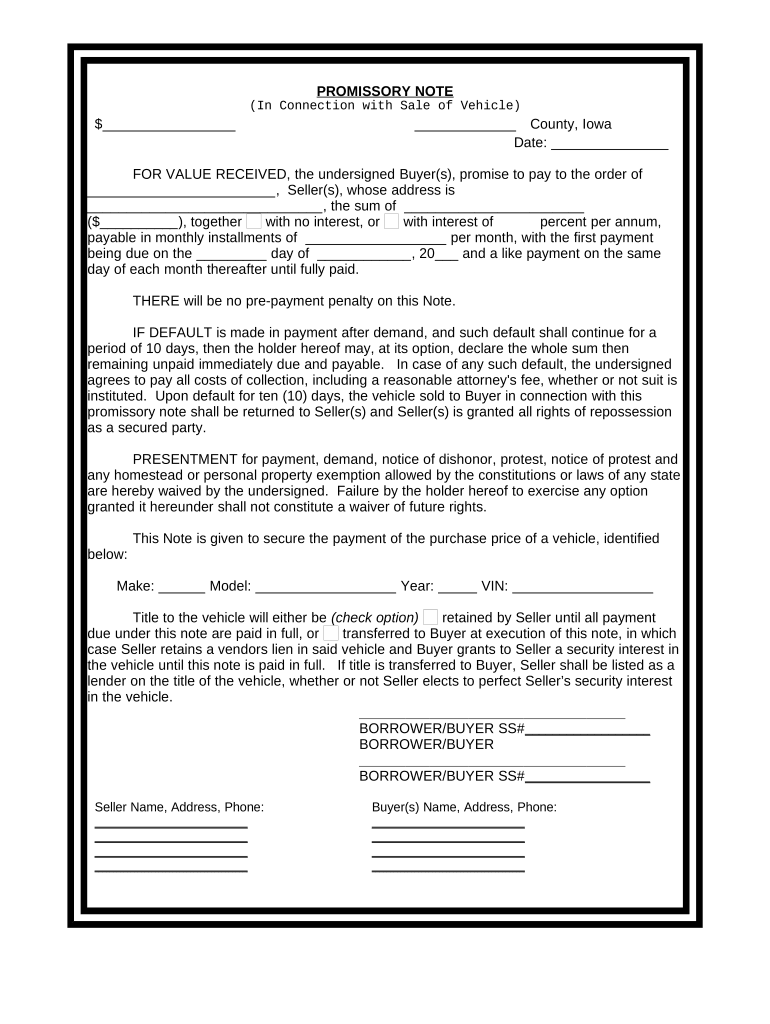

Begin by entering the total amount of the loan in the space provided for '$_____'. This is the sum you are promising to pay.

Fill in the county and date at the top of the form. Ensure that this reflects your current location and the date of signing.

In the section labeled 'FOR VALUE RECEIVED', input the seller's name and address, followed by the payment amount and interest details. Specify if there will be no interest or include a percentage if applicable.

Indicate monthly installment amounts and due dates for payments. Make sure these align with your financial planning.

Complete vehicle details including make, model, year, and VIN in the designated fields to ensure proper identification.

Decide on title retention options by checking either box regarding whether the seller retains title until full payment or transfers it immediately.

Finally, have all buyers sign at the bottom, providing their Social Security numbers as required.

Start using our platform today to easily complete your Promissory Note for free!

Fill out Promissory Note in Connection with Sale of Vehicle or Automobile - Iowa online It's free

Promissory note in connection with sale of vehicle or automobile iowa samplePromissory note in connection with sale of vehicle or automobile iowa examplePromissory note in connection with sale of vehicle or automobile iowa formFree promissory note for vehicle purchasePromissory note for car PDFBill of sale with promissory Note for automobileVehicle promissory noteBill of Sale With payment plan PDF

Security and compliance

At DocHub, your data security is our priority. We follow HIPAA, SOC2, GDPR, and other standards, so you can work on your documents with confidence.

by RF Guthrie 2019 shall be no holder in due course of a promissory note executed with the contract; 27 (3) unless the buyer had notice of an assignment of the con- tractRead more

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.