How to make a living trust without a lawyerLiving trust vs willMichigan trust filing requirementsMichigan trust beneficiary rightsHow much does a trust cost in MichiganWhat is a revocable living trustMichigan trust documentsLiving trust forms michigan

Security and compliance

At DocHub, your data security is our priority. We follow HIPAA, SOC2, GDPR, and other standards, so you can work on your documents with confidence.

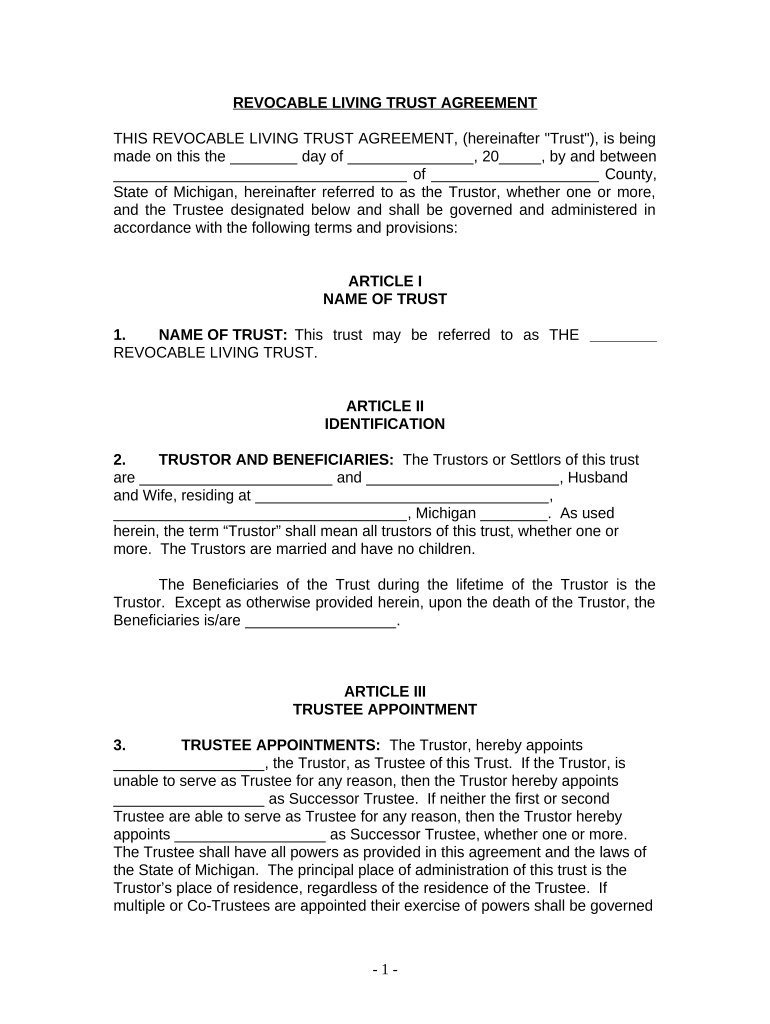

in both the living trust and the testamentary trust. $450,000 for each of the husbands and wifes of the wife and children in any emergency that arises,.

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.