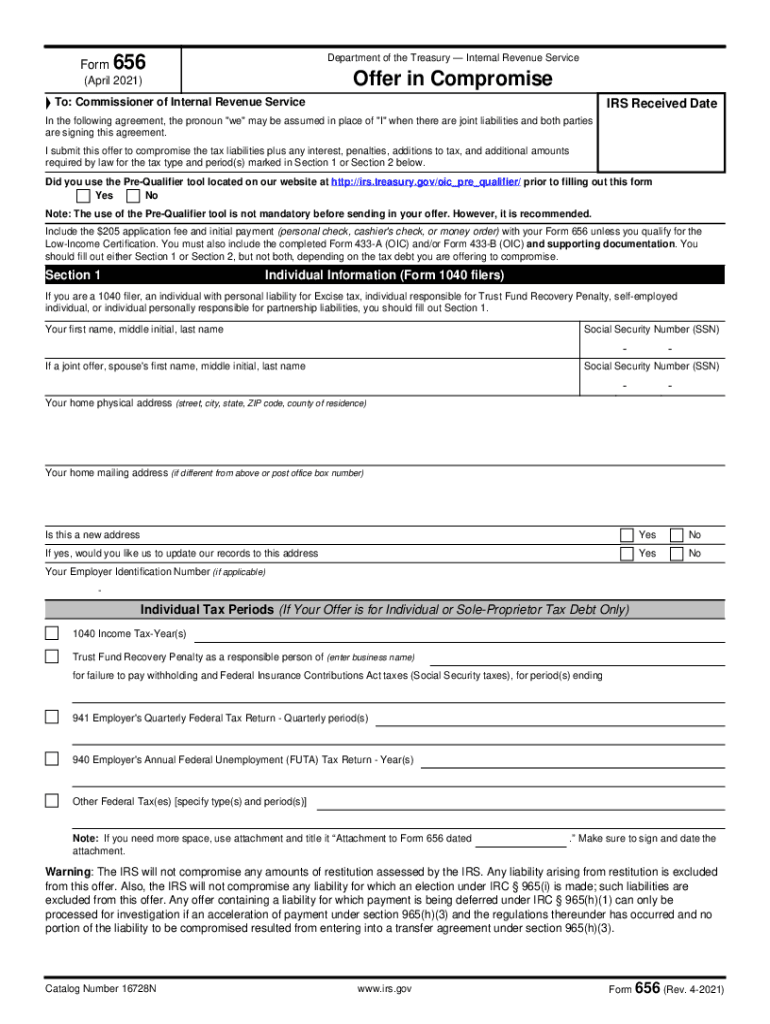

Definition & Purpose of IRS Form 656

IRS Form 656, known as the Offer in Compromise (OIC), is utilized by taxpayers to propose a settlement to the IRS that is less than the full owed tax debt. This form allows individuals and businesses to negotiate tax liabilities based on their financial capability to pay. Essentially, the form is a tool for taxpayers under financial distress who cannot pay their full tax obligations due to their current economic situation.

Key Considerations of the Offer in Compromise

- The IRS evaluates the taxpayer's income, expenses, asset equity, and future earning potential to determine eligibility.

- Submitting Form 656 can halt collection activities as the IRS reviews the offer.

- Approval depends on proving that the offered amount is the maximum collectible under your financial circumstances.

How to Obtain IRS Form 656

Access and Availability

IRS Form 656 can be accessed and downloaded directly from the Internal Revenue Service (IRS) website. Alternatively, you can acquire the form from a local IRS office. It forms part of the Offer in Compromise Pre-Qualifier Tool, which helps you determine preliminary eligibility.

Delivery Options

- Online: Downloadable from IRS.gov in PDF format.

- In Person: Available at IRS Taxpayer Assistance Centers.

- By Request: Mailed upon request through the IRS customer service helpline.

Steps to Complete IRS Form 656

Preparing Your Application

- Gather Financial Records: This includes income statements, expense reports, and records of assets and liabilities.

- Determine the Offer Amount: Calculate a realistic offer by assessing your financial capability.

- Complete Required Accompanying Forms: Submit financial information using Form 433-A (individuals) or Form 433-B (businesses).

Filling Out the Form

- Provide accurate personal information, including social security numbers and contact details.

- Detail your financial situation, including all assets, liabilities, and income sources.

- Specify the payment terms proposed in your offer, whether a lump sum or periodic payments.

Eligibility Criteria for IRS Form 656

Necessary Conditions

- Demonstrated financial inability to pay the full tax liability.

- Submission of all required tax returns and estimated tax payments.

- Compliance with filing requirements for the fiscal year.

Exclusions

- Taxpayers currently in an open bankruptcy proceeding are generally ineligible.

- Companies still non-compliant with filing and payment obligations for payroll and employment taxes.

Required Documents for Submission

Essential Documentation

- Completed Form 656 including Form 656-B for additional information.

- Financial forms 433-A or 433-B showcasing your economic situation.

- Payment of applicable fees and initial payment based on offer terms.

Supporting Financial Details

- Bank statements, pay stubs, and proof of income.

- Documentation of living expenses, such as rental agreements or utility bills.

Filing Deadlines and Important Dates

Timeframes for Submission

While there isn't a strict deadline for submitting IRS Form 656, timely response to any IRS inquiries or additional documentation requests is crucial. Offers are reviewed continuously throughout the year.

Key Considerations

- Ensure all forms and supportive documentation are recent and accurately reflect your current financial status.

- Avoid delays by double-checking that all submission requirements are fulfilled.

IRS Guidelines and Compliance

Adherence to IRS Instructions

Form 656 adheres to the IRS guidelines outlined in the associated publication 1854. The guidelines offer detailed instructions on filling out the form, calculating the offer, and understanding approval criteria.

Compliance and Regulations

- Adhere to the procedures laid down in the IRS manual for processing offers.

- Keep a record of all communications, submissions, and correspondence with the IRS during the process.

Types of Taxpayer Scenarios

Different Types of Applicants

- Individuals: Typically use IRS Form 656 to settle personal income tax debts when facing severe financial hardship.

- Businesses: Small business entities can apply for an OIC to address unpaid corporate taxes or payroll tax debts.

- Retirees and Self-Employed Individuals: Often apply due to fixed or unstable incomes that impact their ability to fulfill tax obligations.

Penalties and Consequences of Non-Compliance

Risks of Incorrect Filing

Non-compliance or inaccurate filings can lead to various penalties, including continued accumulation of interest, rejection of the offer, and potential enforced collection actions by the IRS. Assess each component of the submission thoroughly to mitigate risks.

Consequences of Default

Upon acceptance, any default on agreed payment terms can lead to the revocation of the compromise agreement and reinstatement of the original tax liability. Regular monitoring and adherence to payment schedules are essential.

Use Cases for IRS Form 656

Practical Applications

- Financial Distress: Individuals undergoing significant life changes, such as job loss or medical emergencies, may benefit.

- Business Recovery: Businesses unable to pay outstanding taxes due to downturns in financial performance.

- Debt Resolution Strategy: Employed as part of broader financial planning for debt restructuring.

This comprehensive structure of IRS Form 656 details the critical aspects of its purpose, application, eligibility criteria, and relevant scenarios that apply to taxpayers seeking relief from tax debt obligations.