Sample letter denying creditLetter denying credit templateLetter denying credit car loanLetter denying credit redditLetter denying credit chaseWhat is credit denial in high schoolTitle 15 subsection 16 11 false and misleading denial of my own creditReasons for credit denial

Security and compliance

At DocHub, your data security is our priority. We follow HIPAA, SOC2, GDPR, and other standards, so you can work on your documents with confidence.

What can I do if my credit application was denied because

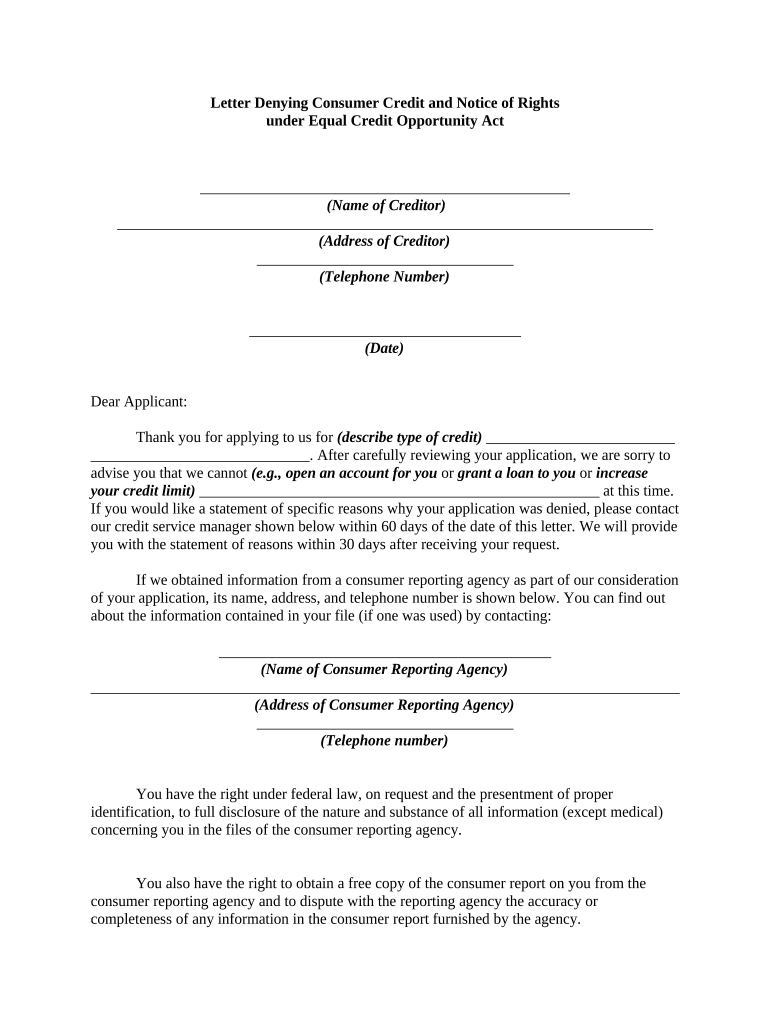

Feb 20, 2026 If you were turned down for a loan or a line of credit, the lender is required to give you a list of the main reasons for its decision.Read more

1. To correct a credit report, you must contact the consumer-reporting agency listed on the denial letter that was sent to you by Direct Loans.Read more

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.