01. Edit your partnership buyout alternatives online

Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send business partner buyout calculator via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out partnership buyout with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open the partnership buyout document in the editor.

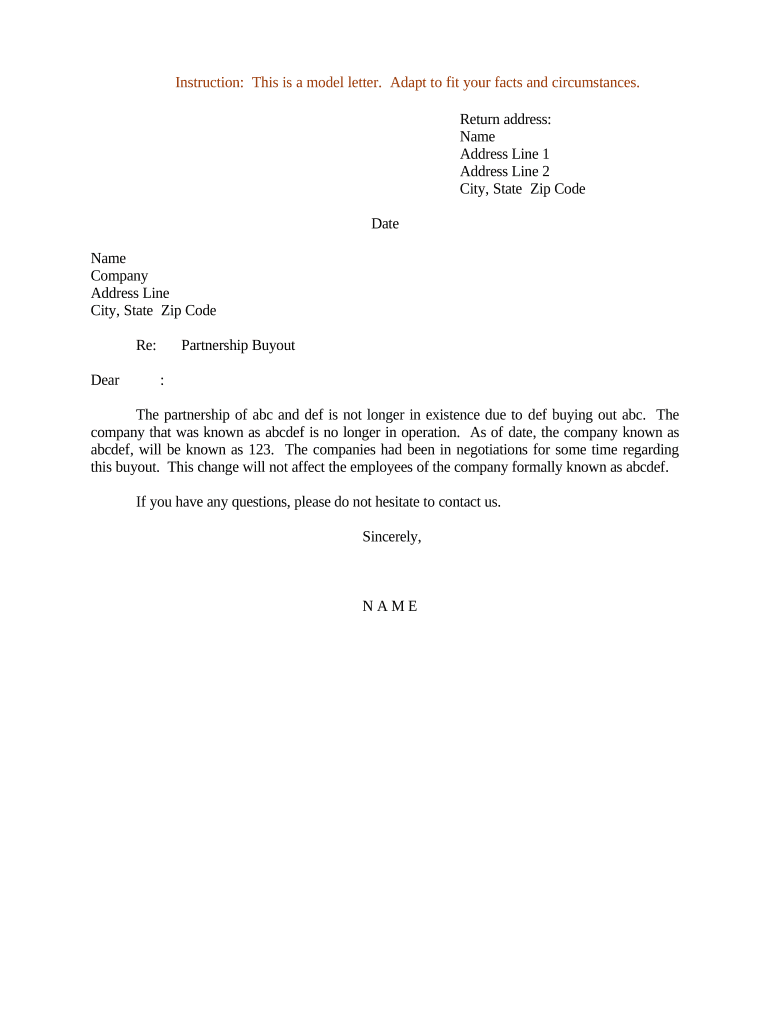

Begin by entering your return address at the top of the form. Include your name, address line 1, address line 2, city, state, and zip code.

Next, input the date of the letter. This is crucial for record-keeping and legal purposes.

Fill in the recipient's details below the date. Include their name, company name, address line, city, state, and zip code.

In the body of the letter, clearly state that the partnership is no longer in existence due to a buyout. Specify which parties are involved and any relevant details about the transition.

Conclude with a professional closing statement and include your name at the bottom of the letter.

Start using our platform today to streamline your partnership buyout process for free!

A partnership dissolution agreement is a legal document that outlines the terms and conditions under which partners agree to terminate their businessRead more

SBA-backed Financing Fuels Growth with Partner Buyout

Working with Choice Bank in 2018, he used an SBA-backed loan to finance the partner equity buy-out. Then in 2020, with the impacts of the COVID-19 crisis, likeRead more

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.