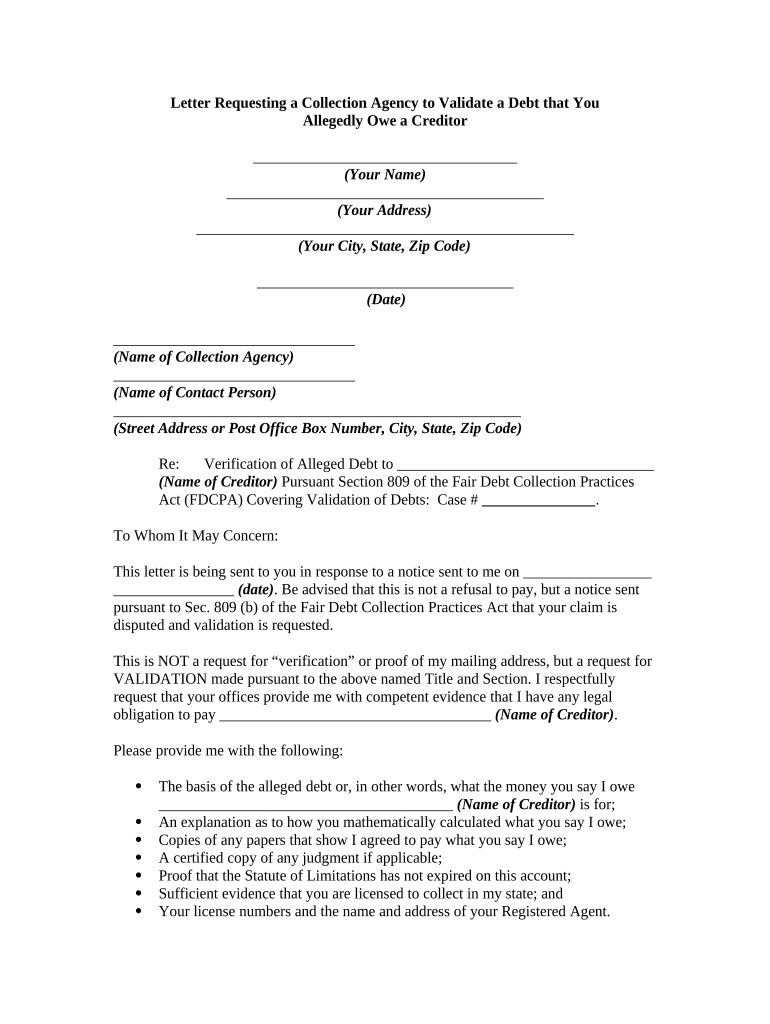

Definition and Purpose of a Debt Validation Letter

A debt validation letter is a formal request sent to a collection agency, asking for verification of an alleged debt. This process is rooted in the Fair Debt Collection Practices Act (FDCPA), which grants consumers the right to dispute a debt and request verification. The letter serves to clarify the validity of the debt, ensuring that consumers are not held accountable for debts they do not owe.

Key Objectives of the Debt Validation Letter

- Dispute Claims: A debtor can formally dispute the debt, asking the collector to provide evidence of the claim.

- Request Detailed Information: Consumers have the right to request documentation showing the debt's origin, balance, and any agreements.

- Warn Against Legal Actions: The letter can warn the collector about potential legal recourse for inaccuracies or failure to comply.

How to Use a Debt Validation Letter

Utilizing a debt validation letter effectively requires a clear understanding of its components and delivery process. This ensures the collection agency complies with your request and provides the necessary information regarding the debt.

Steps to Employ the Debt Validation Letter

- Draft Your Letter: Create a clear and concise letter outlining your request for debt validation.

- Provide Necessary Details: Include your full name, address, and any reference numbers related to the debt.

- Specify Your Request: Clearly state that you are requesting verification of the debt, including details on the original creditor and the amount owed.

- Send the Letter: Mail it to the collection agency using certified mail to ensure there is a record of your request.

- Wait for a Response: The agency must respond within a specified time frame; typically within thirty days.

Important Elements of a Debt Validation Letter

In drafting a debt validation letter, certain key components must be included to ensure that the request adheres to legal standards while maximizing clarity.

Essential Components to Include

- Your Identification Details: Include your name, address, and contact information.

- Agency’s Information: Address the letter to the specific collection agency, including their name and address.

- Reference Information: Mention any account number or reference number associated with the debt.

- Statement of Dispute: Clearly indicate that you are disputing the debt claim and request validation.

- Legal References: Mention the Fair Debt Collection Practices Act, specifying your rights under this law.

Common Reasons for Sending a Debt Validation Letter

Understanding when and why to send a debt validation letter is crucial for consumer advocacy. Various scenarios may prompt an individual to draft such a letter.

Typical Situations for Sending a Validation Letter

- Receiving a Collections Notice: Upon receiving an unfamiliar collection notice, a validation letter requests proof of the debt's validity.

- Inaccuracy in Debt Information: If the consumer identifies discrepancies in the information provided, seeking verification becomes necessary.

- Uncertainty about the Original Creditor: When the creditor named by the collector differs from the consumer’s records, a validation request can clarify the matter.

Legal Use of the Debt Validation Letter

Understanding the legal foundation of a debt validation letter is critical for both consumers and collection agencies. This knowledge ensures compliance with laws and protects consumer rights.

Legal Framework Governing Debt Validation

- Fair Debt Collection Practices Act (FDCPA): This federal law establishes guidelines that collection agencies must follow, including providing verification upon request.

- Consumer Rights: Consumers have the right to dispute debts, request validation, and be protected from unfair collection practices.

- Collection Agency Obligations: Agencies are required to cease collection activities until verification is provided if requested by the consumer.

Free Debt Validation Letter Templates

For those wishing to send a debt validation letter without constructing it from scratch, a template can streamline the process. Various free printable templates are available that align with legal requirements while being user-friendly.

Benefits of Using a Template

- Time-Saving: Templates allow for quicker preparation of the letter.

- Structure: A well-structured template ensures all necessary elements are included.

- Accessibility: Many free debt verification letter templates can be easily downloaded in PDF or DOC formats for immediate use.

Implications of Not Using a Debt Validation Letter

Failing to utilize a debt validation letter can have significant ramifications for consumers. Ignoring such correspondence or not formally disputing a debt could lead to potential consequences.

Consequences of Not Responding

- Legal Judgments: Ignoring collection attempts may result in a default judgment against the consumer.

- Credit Report Impact: Unvalidated debts can negatively affect credit scores and reports.

- Continued Collection Harassment: Without formal dispute, collection agencies may continue aggressive collection efforts.

Practical Examples of Using Debt Validation Letters

Real-world scenarios can often illuminate the importance and use of debt validation letters. Observing these scenarios helps individuals understand when and how to apply such letters effectively.

Scenarios Illustrating Debt Validation

- Unknown Debt from a Collection Agency: A consumer receives a notice for a debt they do not recognize and sends a validation letter.

- Incorrect Amount Listed: After examining a bill, a debtor finds an inflated figure and utilizes a validation letter to question this discrepancy.

- Debt Sold to a Different Agency: After discovering their debt was sold to another agency, a consumer sends a validation letter to the new collector to ascertain full details.