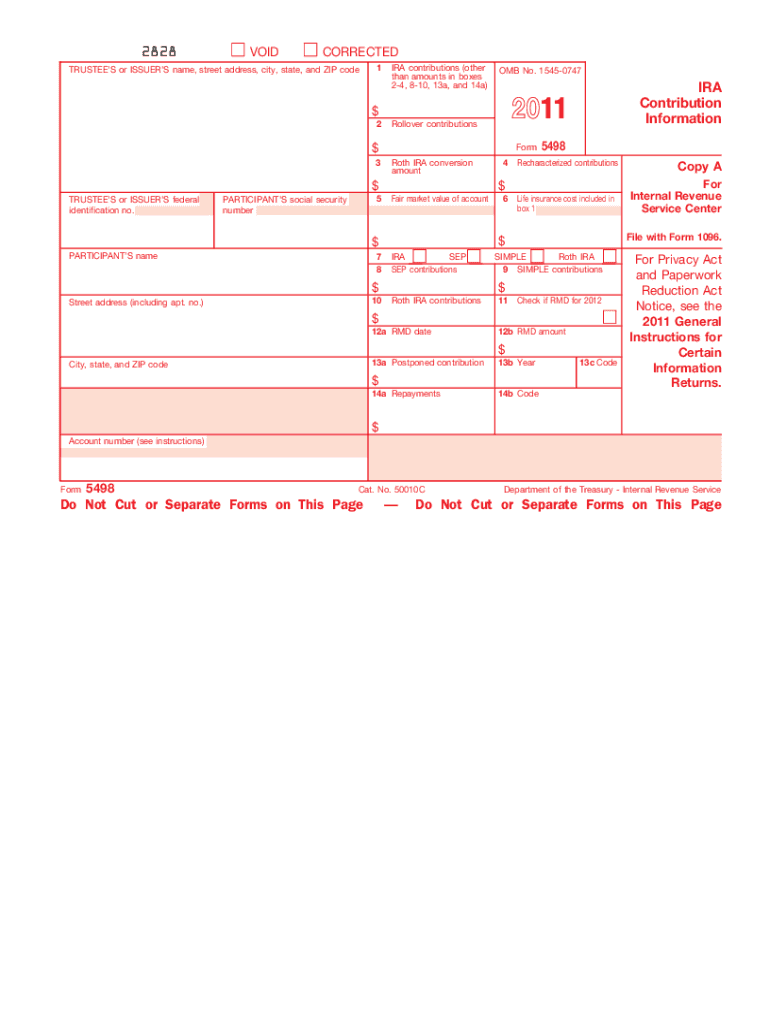

Definition and Purpose of Form 5498

Form 5498 is utilized to report contributions made to individual retirement arrangements (IRAs) within a given tax year. This form collects and details contributions, rollovers, Roth conversions, Fair Market Value (FMV) of the account, and required minimum distributions (RMDs) for traditional IRA holders. While the document can be distributed to participants, it is not directly filed with the IRS due to potential scanning complications. This ensures clear communication between financial institutions and account holders regarding the status and movements of funds in retirement accounts.

Importance of Form 5498

Understanding the significance of Form 5498 is vital for individuals managing retirement accounts, as it ensures proper documentation of all contributions and rollovers into IRAs. Using this form helps account holders maintain compliance with IRS regulations and provides a clear record of financial activities within these accounts. The document serves as a crucial piece of the financial puzzle, helping both taxpayers and financial authorities verify that contributions are within allowed limits and that required minimum distributions are accurately reported.

Steps to Complete Form 5498

Completing Form 5498 involves several precise steps. The trustee or custodian of the IRA is responsible for completing and filing this form. Key steps include:

-

Gathering Required Information: Collect necessary data about the account holder, including their name, address, and Social Security Number (SSN).

-

Detailing Contributions: Accurately document all contributions made to the account during the tax year. This includes regular contributions, rollovers, and any Roth conversions.

-

Reporting FMV: Calculate and report the Fair Market Value of the IRA as of December 31 of the reporting year.

-

Including RMD Information: For participants aged 70½ and older, specify the required minimum distribution.

-

Review and Submit: Check all sections for accuracy before sending the form to the account holder and electronically filing it with the IRS.

How to Obtain Form 5498

IRA account holders typically receive Form 5498 from their trustees or custodians. The form should be distributed by May 31 following the tax year in question. Account holders may also request digital copies from their financial institutions, leveraging online banking services to access and store these documents securely.

Who Typically Uses Form 5498

Form 5498 is primarily used by custodians or trustees managing IRAs, as well as the account holders themselves. Key users include:

-

IRA Holders: Individuals who contribute to traditional IRAs, Roth IRAs, SEP IRAs, or SIMPLE IRAs during the tax year.

-

Financial Institutions: Entities responsible for managing these accounts and ensuring proper documentation and IRS compliance.

-

Certified Public Accountants (CPAs): Professionals assisting clients with their tax filings and ensuring accurate financial record-keeping.

Key Elements of Form 5498

Several critical components must be carefully completed on Form 5498:

-

Account Holder Information: Correctly listing the name, address, and SSN of the account holder.

-

IRA Contributions: Documenting all types of contributions made to the IRA.

-

FMV: Stating the account's Fair Market Value at the end of the year.

-

RMDs: Indicating the RMD for applicable account holders.

Filing Deadlines and Important Dates

It is important to observe deadlines associated with Form 5498. The document must be distributed to IRA account holders by May 31 following the taxable year. Custodians must ensure forms are internally filed with the IRS no later than this date to maintain compliance and avoid penalties. This timeline gives account holders sufficient opportunity to reconcile their records before the federal tax filing deadline.

IRS Guidelines and Regulations

Internal Revenue Service guidelines outline how Form 5498 should be utilized. The form is not sent directly to the IRS by account holders; instead, trustees file it as part of their tax reporting responsibilities. It is vital to adhere to these regulations to avoid discrepancies or potential audits. Understanding IRS rules about contributions, distributions, and rollovers is imperative to properly complete and interpret the document.

Penalties for Non-Compliance

Failing to comply with IRS rules related to Form 5498 can result in significant penalties. Financial institutions may face fines for incorrect or late submissions. Similarly, account holders who fail to verify or dispute information have limited time frames in which to address inaccuracies. Ensuring compliance helps avoid these penalties and maintains accurate and lawful financial conduct.