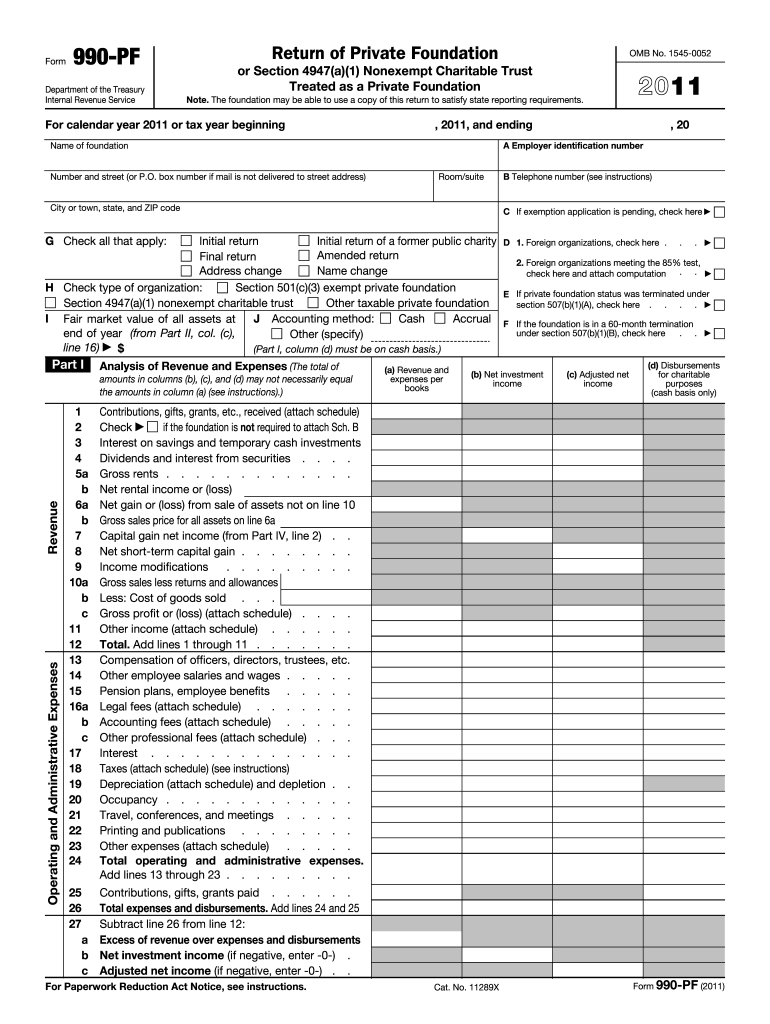

Definition and Purpose of the 2011 990-PF Form

The 2011 990-PF form is an IRS-mandated tax return document required for private foundations and nonexempt charitable trusts. Its primary purpose is to ensure these entities report their financial activities accurately to the US government. The form includes detailed sections for disclosing revenue, expenses, assets, liabilities, and distributions related to charitable purposes.

Key Sections

- Revenue Reporting: Entities must list their total income, including donations and investment earnings.

- Expense Details: This involves itemizing all expenditures, including grants and administrative costs.

- Assets and Liabilities: A snapshot of what the foundation owns versus what it owes.

- Distribution Records: How funds are allocated towards charitable activities.

How to Use the 2011 990-PF Form

Completing the 990-PF form involves several steps and careful attention to detail. It is crucial for compliance with tax regulations and to maintain the entity’s tax-exempt status.

Step-by-Step Process

- Gather Financial Records: Collect all financial statements, donation logs, and expenditure reports from the tax year.

- Complete Basic Information: Fill in details about the organization, including its name, address, and Employer Identification Number (EIN).

- Input Revenue Details: Carefully enter all sources of income received during the year.

- List Expenses: Detail every expenditure, ensuring accuracy to avoid discrepancies.

- Report Assets/Liabilities: Provide the year-end balance of all assets and liabilities.

- Detail Charitable Distributions: Explain how funds were used to support charitable missions.

Obtaining the 2011 990-PF Form

Accessing the 990-PF form is straightforward and can be done through several methods.

Where to Find the Form

- IRS Website: The most direct source, where you can download the form as a PDF.

- Tax Software: Programs like TurboTax often have integrated forms for easy access.

- Professional Accounts: Engaging a tax professional who can provide and fill out the form efficiently.

Key Elements of the 2011 990-PF Form

Understanding the components makes it easier to accurately complete this form:

- Part I: Focuses on revenue and expenses.

- Part II: Reports balance sheets.

- Part III: Lists any charitable activities undertaken.

- Parts IV & V: Encourage detailed compliance narratives.

IRS Guidelines for 2011 990-PF Form

The IRS provides specific guidelines to ensure correct form submission.

Compliance Requirements

- Accuracy: All information must be true and correct.

- Deadline Adherence: The form must be filed by the 15th day of the fifth month after the organization's fiscal year ends.

- Record Retention: Keep copies of the filed form for reference and audits.

Filing Deadlines and Important Dates

Timeliness is critical when submitting the 990-PF form to avoid penalties.

Important Dates

- Filing Deadline: May 15 if the fiscal year follows the calendar year.

- Extensions: Possible extensions can be requested, granting additional time if needed.

Penalties for Non-Compliance

Failure to comply with the 990-PF filing requirements can result in significant penalties.

Potential Consequences

- Financial Penalties: Daily monetary fines until the form is properly submitted.

- Revocation Risks: For repeated avoidance, loss of tax-exempt status is possible.

Legally Binding Use of 2011 990-PF Form

Correct completion and submission ensure ongoing compliance and legal standing.

Legal Considerations

- Data Accuracy: Misreporting can lead to legal liabilities.

- Auditable Records: Maintain integrity with comprehensive and transparent reporting.

By methodically completing each section per IRS instructions, private foundations and trusts protect their interests while maintaining compliance with federal tax obligations. Understanding the importance and execution of the 2011 990-PF form is crucial for continued non-profit operations within the legal tax structure of the United States.