Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send irs form 5227 pdf via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out the 5227 IRS with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open the 5227 IRS in the editor.

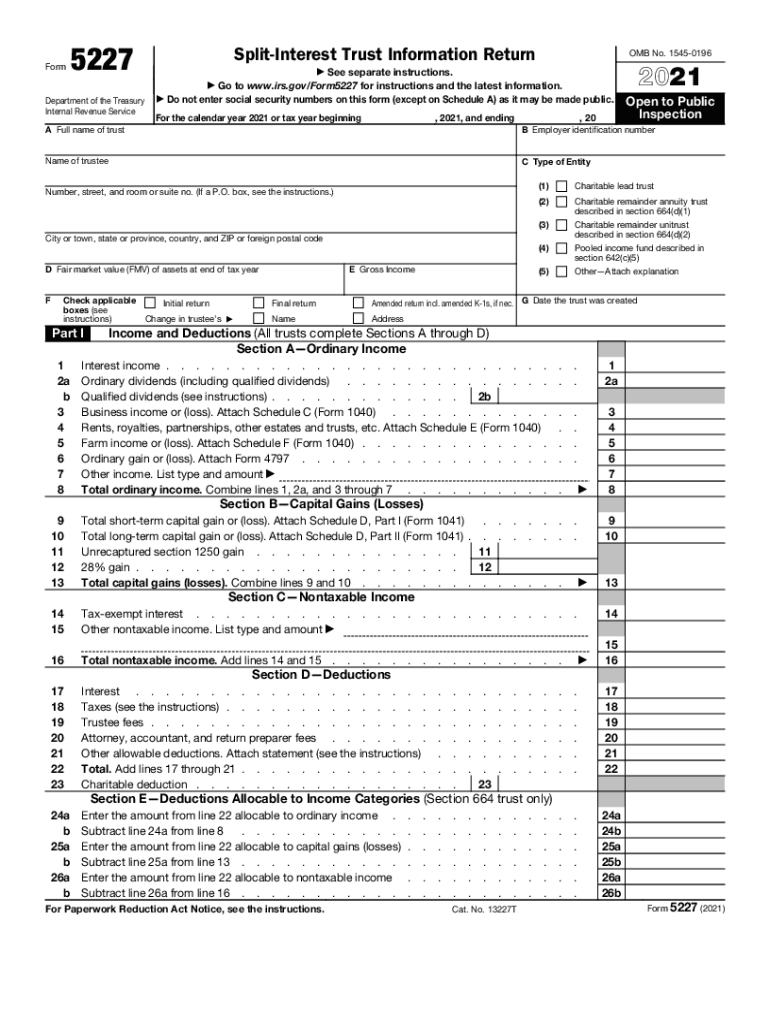

Begin by entering the full name of the trust and its employer identification number in Section A. Ensure accuracy as this information is crucial for identification.

In Section B, report gross income by filling out each applicable field, including interest income and ordinary dividends. Attach any necessary schedules for detailed reporting.

Proceed to Section C to list nontaxable income. This includes tax-exempt interest and any other relevant amounts. Summarize totals accurately.

Complete Section D by detailing allowable deductions such as trustee fees and attorney costs. This will help in calculating net investment income.

Finally, review all entries for completeness and accuracy before saving your work. Utilize our platform’s features to sign and distribute the completed form seamlessly.

Start using our platform today to simplify your form completion process for free!

Complete if the organization is a section 501(c)(3) organization or a section 4947(a)(1) nonexempt charitable trust. Attach to Form 990 or Form 990-EZ. Go toRead more

About Form 5227, Split-Interest Trust Information Return

Mar 30, 2026 Use Form 5227 to: Report the financial activities of a split-interest trust. Provide certain information regarding charitable deductions andRead more

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.