Definition and Purpose of Form 3520

Form 3520, officially titled "Annual Return To Report Transactions With Foreign Trusts and Receipt of Certain Foreign Gifts," is a critical reporting document required by the Internal Revenue Service (IRS). It serves a dual purpose: reporting transactions involving foreign trusts and disclosing the receipt of significant foreign gifts by U.S. persons. The primary goal of this form is to ensure compliance with U.S. tax regulations concerning foreign financial interests and to prevent tax avoidance related to undeclared income or assets abroad. Understanding its implications is crucial for maintaining good standing with tax authorities.

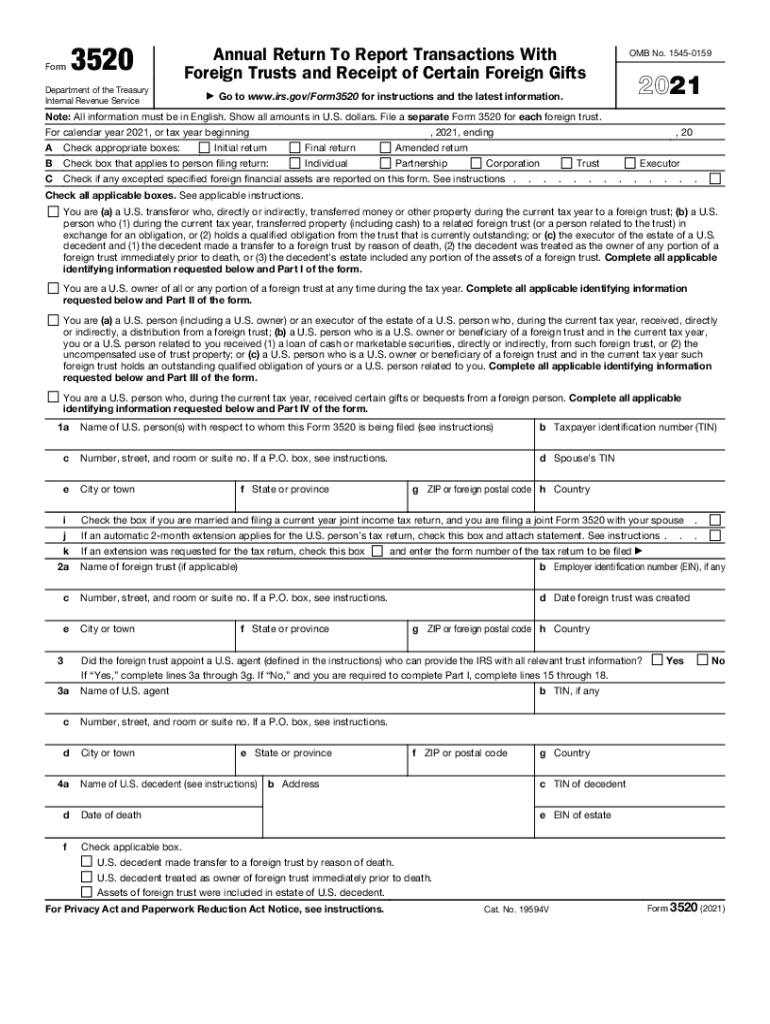

Key Elements of Form 3520

Understanding the key elements of Form 3520 is essential for accurately completing it. The form is divided into distinct sections, each designed to capture different aspects of foreign financial interactions:

- Part I: Identifying information about the filer and their relationship to any foreign trusts.

- Part II: Detailed information about the foreign trust, including transfers to and ownership of the trust.

- Part III: Information about distributions received from a foreign trust.

- Part IV: Disclosure of foreign gifts and bequests received, including the identity of the foreign donor and the gift's value.

Each section requires specific disclosures, so careful attention to these elements ensures compliance and accurate reporting.

Steps to Complete Form 3520

Completing Form 3520 involves a sequential approach to gathering and verifying information. Following these steps ensures thoroughness and accuracy:

- Collect Personal and Foreign Trust Information: Gather all identifying details, including foreign trust names, addresses, and dates of transaction.

- Detail the Trust Transactions: Document all transactions, including transfers of property or funds to foreign trusts.

- Report Foreign Gifts and Bequests: Record any foreign gifts received, ensuring accurate value representation and donor identification.

- Verify Income Calculations: Ensure all income related to foreign trusts or gifts is correctly calculated and reported.

- Review and Double-Check Entries: Before submitting, review the entire form for accuracy and completeness to prevent discrepancies.

- Sign and Date the Form: This seals its validity and confirms the accuracy of the provided information.

Filing Deadlines and Penalties

Form 3520 has specific deadlines linked to the filer's tax return due date, usually aligning with April 15 for most taxpayers. Filing this form timely is crucial to avoid penalties, which can be substantial. Late filing or failing to report incur penalties up to 35% of the gross reportable amount. Therefore, understanding filing deadlines and adhering strictly to them is vital for compliance. Extensions for filing these returns can sometimes coincide with approved income tax extensions, providing some leeway in complex situations.

Required Documents for Form 3520

Preparation and accurate completion necessitate having all related documents on hand. Essential documents include:

- Trust deeds and legal documents: to confirm ownership and terms.

- Statements of income related to trust transactions: these ensure all reportable income is captured.

- Documentation of received foreign gifts: this includes valuation proofs and letters or agreements from the donor.

Organizing and categorizing these documents simplifies the process of form completion and supports accuracy.

Who Typically Uses Form 3520

Form 3520 is typically required by a specific group of U.S. individuals and entities:

- U.S. citizens and residents: who have engaged in transactions with foreign trusts or received foreign gifts.

- Executors of estates: tasked with handling foreign assets or bequests within an estate.

- Businesses and entities, including partnerships and corporations: with ties to foreign trusts or that receive substantial foreign gifts.

The form's necessity arises across a range of scenarios where legal U.S. residency intersects with foreign financial interactions.

IRS Guidelines for Form 3520

The IRS provides extensive guidance for completing and submitting Form 3520. Adherence to these guidelines ensures the form meets all IRS requirements and helps avoid common errors. Key recommendations include:

- Detailed record maintenance: Keep meticulous records of any related transactions and corresponding documentation for audit purposes.

- Consultation with tax professionals: Engaging professionals can clarify complex situations and ensure the intricate details of foreign interactions are properly documented.

- Use of IRS resources: Leverage IRS publications and instructions dedicated to foreign gifts and trust reporting to fully comprehend obligations.

Application Process and Approval Time

While Form 3520 requires submission and compliance rather than approval, understanding the processing timeline is helpful. Upon submission, the IRS will process the form to ensure all information aligns with reporting requirements. U.S. persons might receive queries for clarification during the review period, necessitating timely responses to expedite resolution and prevent issues. While there's no "approval" in the traditional sense, comprehensive form completion and adherence to guidelines minimize risks of complications during the IRS's review.