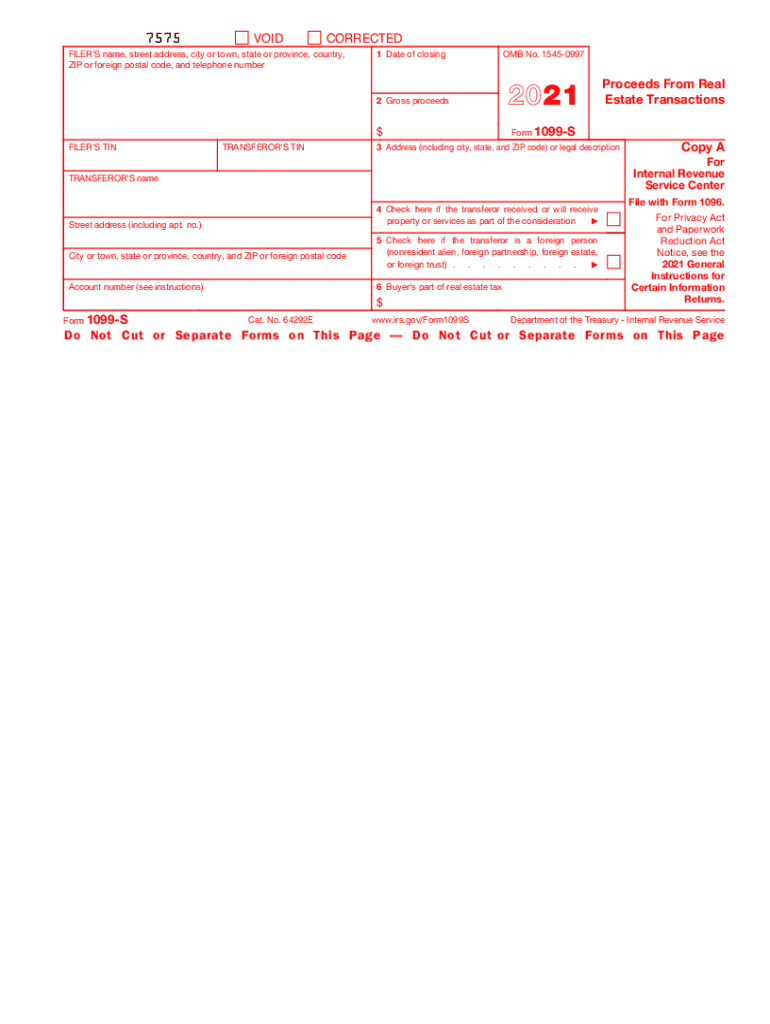

Definition & Meaning

The Form 1099-S is an IRS tax form used for reporting the sale or exchange of real estate properties. This form communicates the proceeds generated from transactions to the IRS. It is typically handled by the person responsible for closing the transaction, often a real estate broker, mortgage lender, or title company. The 2021 version of Form 1099-S captures the transaction details of real estate sales completed in that year. Understanding the fundamental use of this form helps taxpayers ensure compliance and prevent potential issues during tax filings.

Steps to Complete the 1099-S Form 2021

-

Identify the Filer: Include the information of the person responsible for reporting the sale, such as the real estate broker or closing agent.

-

Receive Transferor’s Information: Gather details from the property seller, including their name, address, and taxpayer identification number.

-

Complete Transaction Details: Enter the gross proceeds from the sale and any additional financial amounts pertinent to the closing.

-

Specify Property Details: Record the property location and description to align with IRS requirements.

-

Submit Copy A to the IRS: As per IRS instructions, send Copy A to the IRS and retain other copies for records and distribution to involved parties.

Completing this form accurately is crucial for avoiding penalties and ensuring compliance with federal tax obligations.

Who Typically Uses the 1099-S Form 2021

The primary users of Form 1099-S include:

- Real Estate Brokers and Title Companies: These entities are usually the ones to prepare and file the form since they oversee the closing.

- Property Sellers and Buyers: While not responsible for filing, sellers and buyers need to understand and verify the form details for their own tax records.

- Attorneys and Accountants: Professionals assisting clients in real estate transactions often review the 1099-S form to ensure accuracy and compliance.

These users need to collaborate to ensure the form is completed and submitted accurately, helping maintain transparent and lawful transaction records.

Key Elements of the 1099-S Form 2021

-

Filer Information Box: This section identifies the entity responsible for reporting the transaction.

-

Transferor’s Information Box: Details of the individual or entity selling the property.

-

Gross Proceeds Box: The total amount received from the real estate sale.

-

Property Description Box: Captures detailed information about the location and nature of the sold property.

Understanding these elements is vital for the accurate completion and submission of Form 1099-S, ensuring compliance with IRS regulations.

IRS Guidelines

The IRS provides specific guidelines on how the Form 1099-S should be filled out and submitted. Key guidelines include:

-

Timely Filing: Copy A must be filed with the IRS by the end of February if filing on paper; March 31 for electronic filings.

-

Copies Distribution: Distribute copies to the seller and, if applicable, buyer to ensure all parties are informed of the report.

-

Accuracy is Mandatory: Mistakes can lead to fines; ensuring all information is correct is crucial.

-

Electronic Submission: Encouraged by the IRS for faster and more efficient processing.

Following these guidelines can help prevent errors that might lead to penalties.

Filing Deadlines / Important Dates

-

January 31st: Deadline for providing the form to transferors.

-

End of February: Deadline for paper filing with the IRS.

-

March 31st: Deadline for electronic filing with the IRS.

Ensuring timely filing aligns with IRS requirements and mitigates the risk of penalties for late submissions.

Penalties for Non-Compliance

Failure to comply with the filing requirements of Form 1099-S can result in substantial penalties imposed by the IRS:

-

Late Filing Penalties: Starting at $50 per information return if filed within 30 days after the due date, increasing over time.

-

Intentional Disregard Penalties: Much higher penalties for intentionally failing to file or provide correct information.

Understanding and adhering to filing requirements mitigate the risk of such penalties.

Digital vs. Paper Version

-

Digital Filing: Offers a streamlined process and reduces the risk of errors associated with manual entry. It also provides quicker IRS responses.

-

Paper Filing: Traditional method but can be prone to errors and slower in processing.

-

Advantages of Digital: More eco-friendly, cost-effective, and can easily integrate with accounting software, benefiting those managing large volumes of transactions.

Choosing the right filing method ensures efficiency and compliance, particularly for entities managing multiple transactions.

Software Compatibility

DocHub, TurboTax, and QuickBooks are among the software solutions that facilitate the management of Form 1099-S:

-

TurboTax and QuickBooks: Allow users to integrate form completion with other tax or business functions.

-

DocHub Integration: Enables seamless document import, editing, and signing, streamlining the form completion process, especially for teams working collaboratively.

Selecting compatible software and utilizing it effectively can make tax season less burdensome for filers.