Definition & Purpose of Form 14

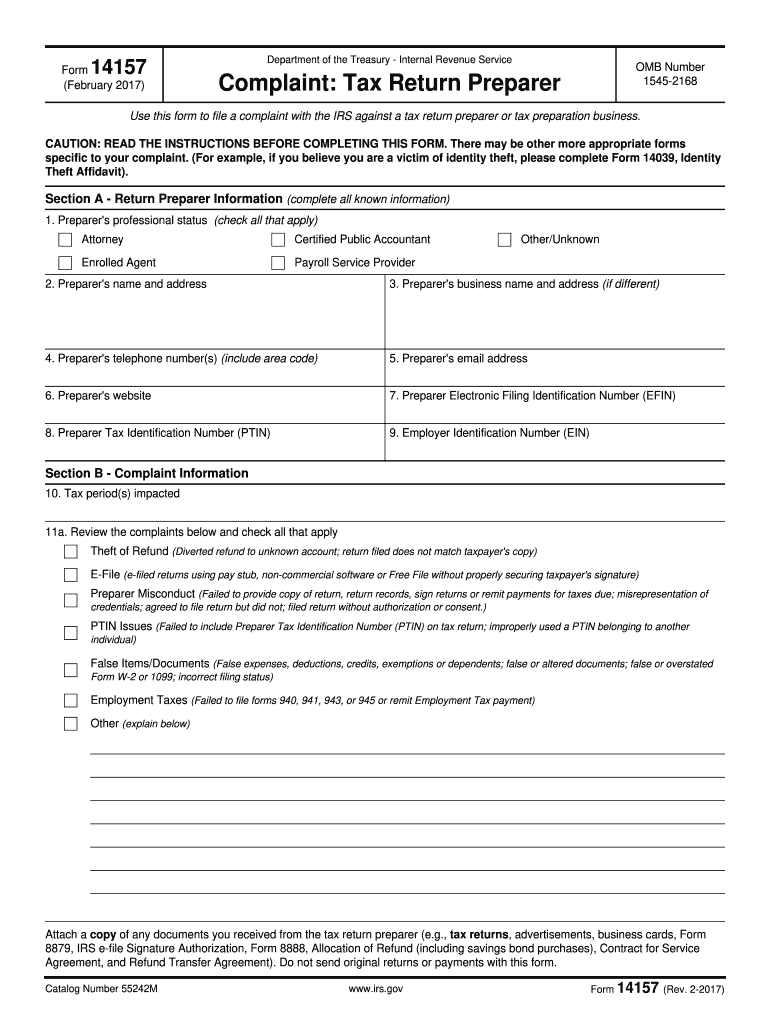

Form 14157 is an official document issued by the Internal Revenue Service (IRS) for reporting misconduct by tax return preparers or tax preparation businesses. Its primary purpose is to allow individuals to file complaints regarding unethical practices such as theft of refunds, filing errors, and submission of false documents. By providing a standardized way to report such issues, the IRS ensures that reports are structured and contain all necessary details. Those using this form are encouraged to provide comprehensive information, such as the preparer's name, business details, and a clear description of the complaint.

How to Use Form 14

To properly use Form 14157, individuals should begin by carefully reading the form instructions, typically included by the IRS. It's important to gather all requisite details related to the complaint before starting the form, such as records of correspondence and any supporting documents. Fill out the form accurately, providing specific examples of misconduct and any corrective measures sought. Once completed, the form must be submitted to the IRS. Knowing how to accurately complete and submit the form is crucial for a productive investigation by the IRS.

Steps to Complete Form 14

-

Gather Necessary Information:

- Collect all pertinent details about the preparer and the incident.

- Assemble any supporting documents, such as tax returns and correspondence.

-

Fill Personal and Preparer Information:

- Input your personal data and that of the tax preparer involved in the misconduct.

-

Detail the Complaint:

- Clearly describe the nature of the complaint, providing specific examples.

- Mention any attempts made to resolve the issue prior to filing the complaint.

-

Review and Attach Documents:

- Ensure that all fields are completed accurately and attach any necessary documents for support.

-

Submission:

- Mail the form and accompanying documents to the appropriate IRS address specified on the form.

Key Elements of Form 14

Form 14157 contains several crucial sections designed to facilitate detailed reporting:

- Preparer's Information: Details about the tax return preparer, including name, business, and contact information.

- Complaint Information: A structured section to describe the incident, including specific acts of misconduct and affected tax years.

- Taxpayer's Information: Details about the taxpayer making the complaint, including their IRS-preferred contact information.

- Supporting Documents: Space to specify and attach relevant documentation or records that support the complaint.

Who Typically Uses Form 14

Individuals who suspect misconduct in the preparation of their tax returns typically use Form 14157. This includes:

- Taxpayers who suspect incorrect filing or unauthorized changes to their return.

- Individuals whose refunds were stolen or misappropriated by the preparer.

- Anyone who faced improper fees or charges not previously disclosed by the preparer.

The form allows affected parties to formally report issues and seek resolution through the IRS, maintaining fairness and integrity in tax reporting.

IRS Guidelines for Form Preparation and Submission

The IRS provides detailed guidelines aimed at ensuring accurate and complete submissions of Form 14157:

- Ensure all sections are accurately completed.

- Use ink or typewritten text for clarity.

- Follow instructions about attaching supporting documents.

- Submit the form within the timeframe specified to ensure it is addressed efficiently.

The IRS web resources offer further insights into any updates or changes in submission procedures, ensuring complainants are well-informed and compliant.

Filing Deadlines and Important Dates

While there is no strict deadline for submitting Form 14157, timely submission is recommended to expedite the investigation process. Taxpayers should file the complaint as soon as misconduct is identified. Keep in mind tax deadlines for filing returns, as this can affect the relevance of the complaint. If timely filing isn't possible, keeping a detailed timeline and record of the incident is useful for future submissions.

Legal Use and Penalties for Non-Compliance

Form 14157 plays a vital role in upholding the law by providing a mechanism to report non-compliance among tax preparers. When the form is used to report misconduct, the IRS can take corrective action, ranging from fines and penalties to disqualifying a preparer from practice. Taxpayers should understand that while filing the form often leads to investigations, it is not an alternative to resolving disputes through legal means, such as lawsuits, if needed. Misuse of the form or fraudulent claims can result in penalties, emphasizing the need for accurate and truthful reporting.