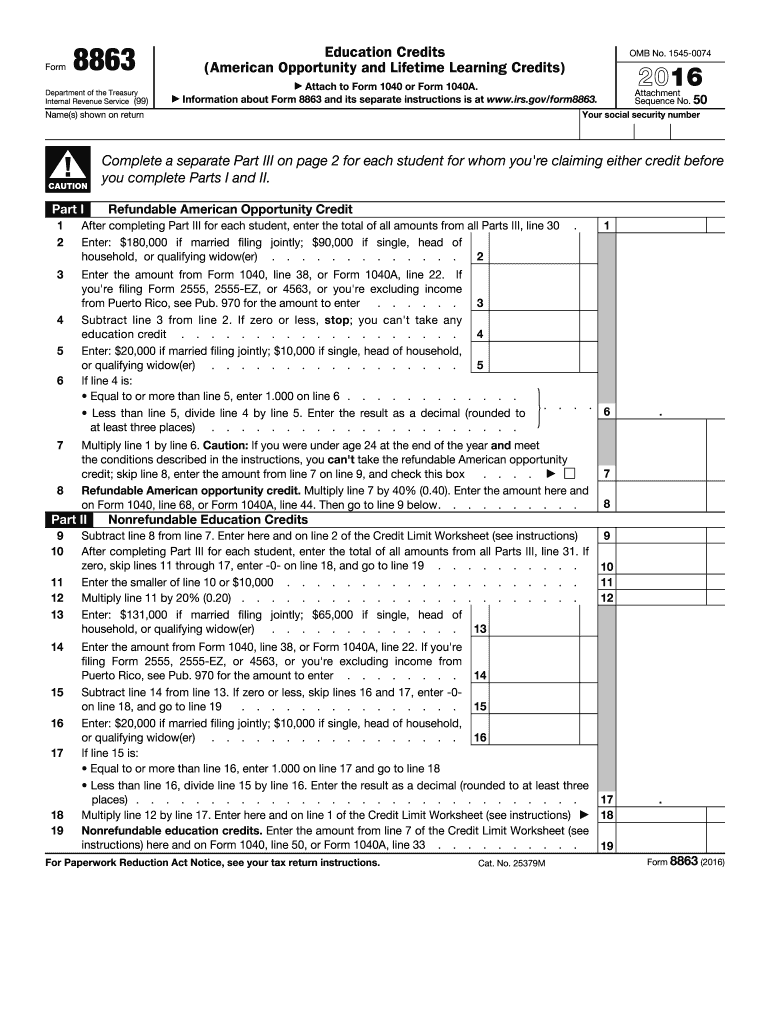

Definition and Purpose of Form 8863

Form 8863, officially titled "Education Credits," is integral to claiming education-related tax credits on U.S. federal tax returns. The primary purpose of this form is to enable taxpayers to claim credits such as the American Opportunity Credit and the Lifetime Learning Credit. These credits aim to alleviate the financial burden of higher education by reimbursing part of qualified educational expenses. The form requires input of student-specific information alongside data pertaining to the educational institution attended. Importantly, this document includes instructions for calculating both refundable and nonrefundable credits, allowing taxpayers to maximize their tax benefits based on eligibility criteria and income limits.

How to Use Form 8863 for Tax Credits

To utilize Form 8863 effectively, taxpayers should begin by understanding the types of education credits it encompasses. The American Opportunity Credit is applicable for undergraduate students enrolled at least half-time and covers tuition, fees, and course materials. In contrast, the Lifetime Learning Credit is available to a broader range of students, including graduate and part-time, focusing predominantly on tuition.

Start by gathering documents like tuition statements (Form 1098-T) and records of any additional qualifying expenses. Input necessary information into corresponding sections of Form 8863, ensuring accuracy to avoid IRS rejections. The form's layout aids in determining the refundable and nonrefundable segments of the credit, breaking down eligibility based on AGI thresholds.

How to Obtain Form 8863

Form 8863 can be obtained electronically from the official IRS website, ensuring accessibility and authenticity of the version used. Tax preparation software also typically incorporates digital versions of the form, streamlining the filing process for tech-savvy users. For those preferring a physical copy, downloading and printing the form directly from the IRS remains a convenient option. Ensure usage of the specific 2016 version if filing retroactively for that tax year, as credit calculations and eligibility criteria may vary annually.

Steps to Complete Form 8863

-

Gather Documentation: Collect form 1098-T from educational institutions and compile records of additional educational expenses.

-

Determine Eligibility: Identify which credits you qualify for—American Opportunity or Lifetime Learning Credit—based on student status and enrollment level.

-

Complete Personal Information: Fill in the initial section with taxpayer identification details and adjusted gross income.

-

Input Education Expenses: Carefully enter tuition and qualified expenses, referencing the 1098-T form for accuracy.

-

Calculate Credits: Use the step-by-step guide on the form to compute both refundable and nonrefundable credits, ensuring adherence to eligibility limits and thresholds.

-

Review and Submit: Double-check entries for errors before submission. Electronic filing via IRS-approved software can streamline the process and potentially reduce processing times.

Key Elements of Form 8863

Understanding the core elements of Form 8863 is essential for accurate completion. It consists of two main parts: Part I addresses refundable American Opportunity Credit components, while Part II focuses on the nonrefundable Lifetime Learning Credit. Each part requires comprehensive information on educational institutions, student details, and exact expense calculations. A credits and income limit worksheet facilitates determining qualification caps for the credits. Thorough comprehension of these elements is crucial to maximize potential tax benefits while ensuring compliance with IRS regulations.

Eligibility Criteria for Education Credits

Eligibility for credits using Form 8863 hinges on various factors, chiefly centered around the student's status and the nature of their educational pursuits. The American Opportunity Credit mandates that students be pursuing a degree, enrolled at least half-time, and that there be no felony drug conviction history. In contrast, the Lifetime Learning Credit is broader, catering to all postsecondary education levels and including courses taken to improve job skills. Moreover, taxpayers should meet financial thresholds, as these credits are phased out for higher income levels, making careful review of income levels and thresholds imperative.

IRS Guidelines for Form 8863

The IRS provides comprehensive guidelines for Form 8863, clarifying nuances of credit eligibility and acceptable expenditure types. Familiarizing oneself with these guidelines is paramount to ensure adherence to regulations. Key areas include definitions of eligible educational institutions, stipulations around qualifying expenses, and detailed descriptions of different credit caps and their phase-out levels. Adhering to IRS guidelines not only prevents errors in filing but also minimizes the risk of audits or penalties.

Required Documents for Filing Form 8863

Accurate completion of Form 8863 requires several crucial documents. Key among these is the Form 1098-T, issued by educational institutions, which summarizes tuition fees and any scholarships received. Additional records may include receipts for textbooks, course materials, and proof of payment for tuition and fees not encompassed by scholarships or grants. Detailed documentation supports the validity of claims and smoothens the filing process, ensuring alignment with IRS substantiation requirements.