First, sign in to your DocHub account. If you don't have one, you can easily register for free.

Once logged in, head to your dashboard. This is your primary hub for all document-based operations.

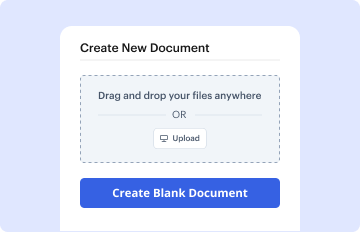

In your dashboard, choose New Document in the upper left corner. Pick Create Blank Document to build the Mortgage Closing Document from the ground up.

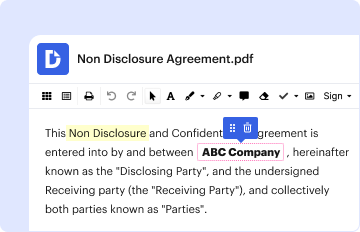

Add numerous fields like text boxes, images, signature fields, and other interactive areas to your form and designate these fields to certain users as required.

Personalize your template by inserting walkthroughs or any other necessary tips utilizing the text feature.

Attentively check your created Mortgage Closing Document for any typos or essential adjustments. Utilize DocHub's editing capabilities to enhance your document.

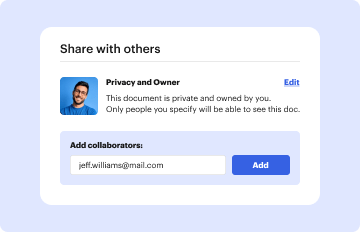

After finalizing, save your work. You may choose to save it within DocHub, transfer it to various storage solutions, or send it via a link or email.