Visit the DocHub website and register for the free trial. This gives you access to every feature you’ll need to create your Accounting Related Legal Form with no upfront cost.

Log in to your DocHub account and go to the dashboard.

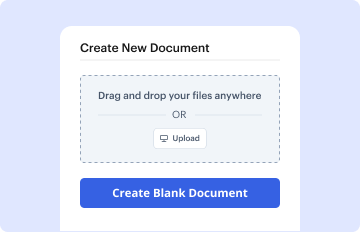

Hit New Document in your dashboard, and choose Create Blank Document to design your Accounting Related Legal Form from the ground up.

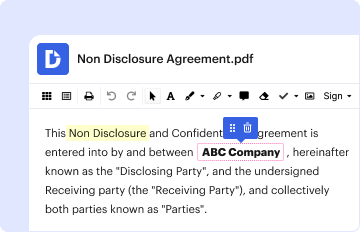

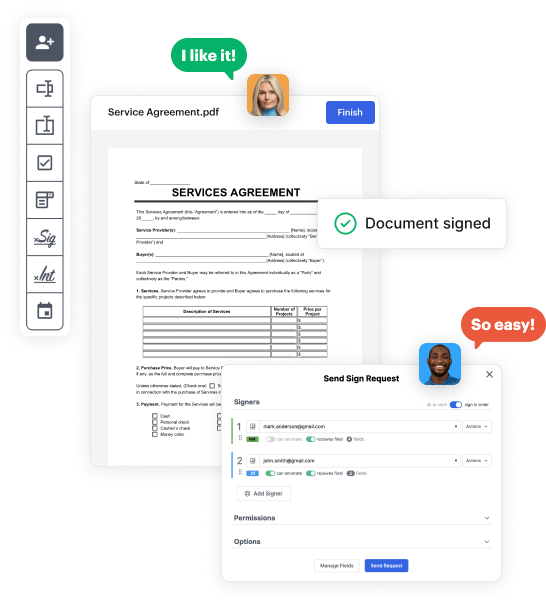

Add various elements such as text boxes, radio buttons, icons, signatures, etc. Organize these elements to match the layout of your document and assign them to recipients if needed.

Rearrange your document effortlessly by adding, moving, deleting, or combining pages with just a few clicks.

Convert your newly crafted form into a template if you need to send many copies of the same document multiple times.

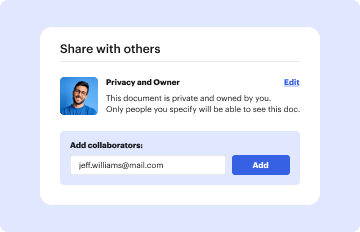

Send the form via email, share a public link, or even post it online if you wish to collect responses from a broader audience.