Start by accessing your DocHub account. Utilize the pro DocHub functionality at no cost for 30 days.

Once logged in, head to the DocHub dashboard. This is where you'll create your forms and manage your document workflow.

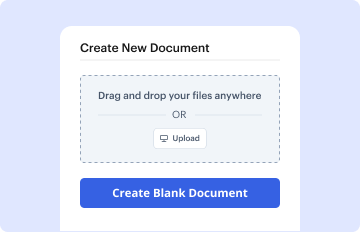

Hit New Document and choose Create Blank Document to be taken to the form builder.

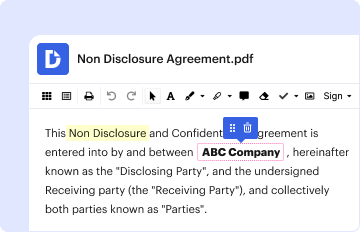

Use the DocHub toolset to add and configure form fields like text areas, signature boxes, images, and others to your document.

Include necessary text, such as questions or instructions, using the text field to assist the users in your document.

Alter the properties of each field, such as making them required or formatting them according to the data you expect to collect. Assign recipients if applicable.

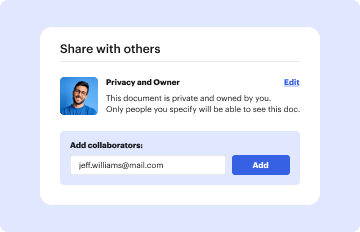

After you’ve managed to design the Allowance for doubtful accounts Balance Sheet Template, make a final review of your document. Then, save the form within DocHub, transfer it to your chosen location, or share it via a link or email.