Start by creating a free DocHub account using any offered sign-up method. If you already have one, simply log in.

Try out the entire set of DocHub's pro tools by signing up for a free 30-day trial of the Pro plan and proceed to build your Mortgage and Loan.

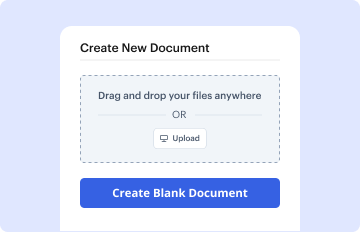

In your dashboard, select the New Document button > scroll down and hit Create Blank Document. You’ll be taken to the editor.

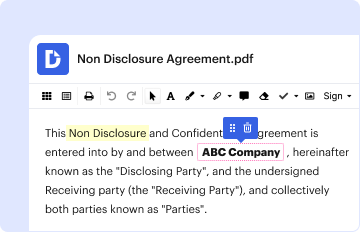

Utilize the Page Controls icon marked by the arrow to toggle between two page views and layouts for more flexibility.

Navigate through the top toolbar to add document fields. Add and format text boxes, the signature block (if applicable), add photos, and other elements.

Configure the fillable areas you incorporated per your preferred layout. Modify each field's size, font, and alignment to make sure the form is user-friendly and polished.

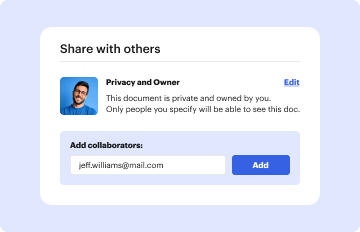

Save the completed copy in DocHub or in platforms like Google Drive or Dropbox, or create a new Mortgage and Loan. Share your form via email or get a public link to reach more people.